As business owners, the landscape and trajectory of your business is always shifting. And if you aren’t regularly reviewing the buy-sell agreement that you have in place for your business, you might not be protected in the way you WANT to be or NEED to be.

This potential gap in the right protection can leave you, your business partners, key employees, and business as a whole susceptible to immense loss.

We know that being a business owner comes with a great deal of responsibility, for not only your business, but your employees and their well-being. Here at Consolidated Planning, we have a team of expert financial advisors dedicated to helping you adequately plan for your business, no matter what that might look like.

Part of planning for your business is addressing your buy-sell structure. As you stand today maybe you don’t have one in place or maybe you haven’t reviewed it since there have been major changes. Here, we will help you understand what an appropriate buy-sell structure looks like, four options for your buy-sell structure, and how you can implement the RIGHT buy-sell structure for your goals.

Why Do You Need A Buy-Sell Structure?

As a business owner, it’s safe to say that you’ve poured an endless amount of time and energy into making your business what it is today. Now, ensuring that you have the best Buy-Sell structure in place for your life’s work just makes sense.

The problem with failing to protect your biggest asset is that your business and the success of it is dependent upon you showing up each and every day. That means upon your exit from the business, the value of the business may be left up in the air. Unlike the value of every other asset on your balance sheet today – cash, investments, 401ks, and real estate, the worth of your business today is not the same value without you in the event of a sudden or involuntary departure.

In fact, your business without you may actually be worth less than the value today, but how much less?

- Less than book value

- Worth zero, or

- Worth LESS than zero

Ensuring your life’s work and the value it represents remains a part of your balance sheet is vital to your financial well being. That’s why you need the best Buy-Sell structure for your biggest asset.

4 Options For Your Buy-Sell Structure

The goal with choosing the right Buy-Sell structure is stability for your business, your business partners and its key employees. Determining your Buy-Sell structure well in advance helps you to be proactive and make clear, thoughtful decisions for the benefit of those after your exit – your family and business partners.

Remember that the best buy-sell structure for your business should align with your objectives, protect the interests of all owners, and provide a clear framework for handling ownership changes.

#1 Cross Purchase Buy-Sell

This Buy-Sell structure is one of the most common agreements between business partners. One of the main reasons for that is the step-up in basis. Because inherited assets can have an appreciated cost, this resets the cost basis for tax purposes. There is no tax on this transaction, making it very appealing for the right business partners. This agreement outlines the terms and conditions under which the owners agree to buy and sell each other’s ownership interests in the event of certain triggering events.

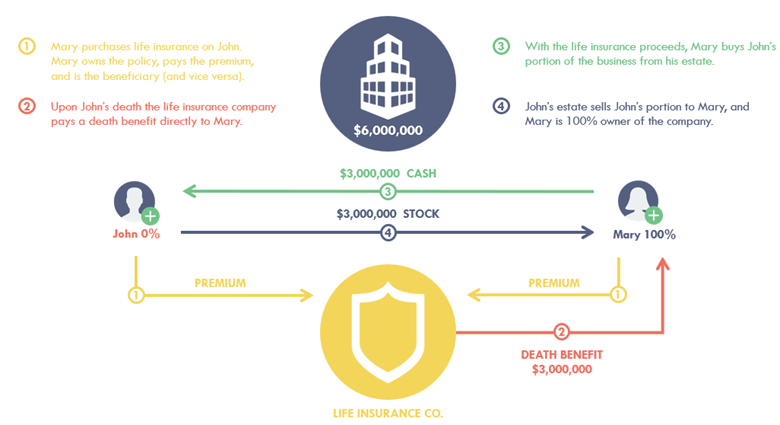

For our example, we’ll use John and Mary. John and Mary each own 50% of a business valued at $6,000,000. The structure of a Cross Purchase Buy-Sell Agreement might look like this:

John buys life insurance on Mary and Mary buys life insurance on John.

John then:

- Owns

- Pays for, and

- Is the beneficiary of Mary’s policy, and

- Vice versa

If John dies, the life insurance proceeds would go to Mary and through the Buy-Sell agreement. Mary is then compelled to purchase John’s ownership in the company from the estate. In this instance, $3,000,000 from the policy to pay his estate. The estate then transfers the money back to Mary.

This Buy-Sell agreement is ideal for John and Mary’s circumstance:

- There are two business owners for a simple strategy

- The surviving owner receives a step-up in tax basis (the adjustment in the cost basis of an inherited asset to its fair market value on the date of the decedent’s death.)

#2 Entity Purchase Buy-Sell

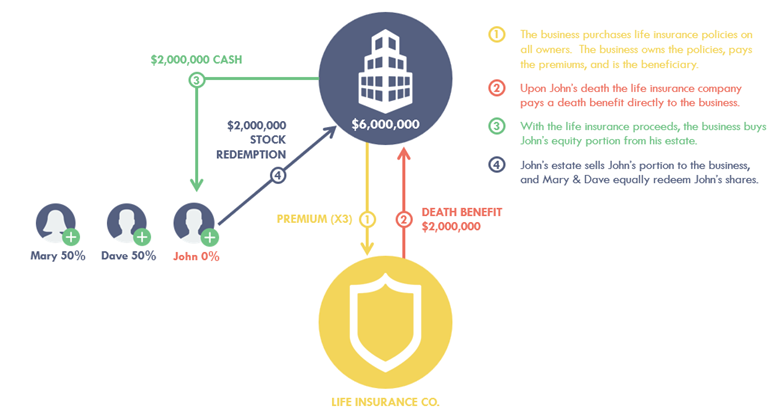

The Entity Buy-Sell Agreement is also called a stock redemption. This agreement is more ideal for a business with multiple owners. As you would probably guess, as the number of business owners increases, so does the complexity of planning.

For our example, we’ll use John, Mary, and Dave each owning 1/3 of a company valued at $6,000,000.

With this structure, the business or entity:

- Owns

- Pays for, and

- Is the beneficiary of all life insurance policies

Under this structure, there are just three policies rather than potentially 6. One policy between the entity and Mary, one policy between the entity and Dave, and one policy between the entity and John. If someone dies, the company receives the life insurance proceeds. Then the company uses the proceeds to buy out the estate, the shares come back into the company and Mary and Dave are 50% owners of the company. The entity redeemed and reabsorbed the shares.

This Buy-Sell agreement is ideal for Mary, Dave, and John’s circumstance:

- There is one policy per owner

- This is easier to administer with 3 or more owners

However, with an Entity purchase, there are a few notable downsides, including:

- There is no step-up in basis, meaning the taxation of these shares moving forward could be greater

- Policies are also exposed to creditors of the business within this structure

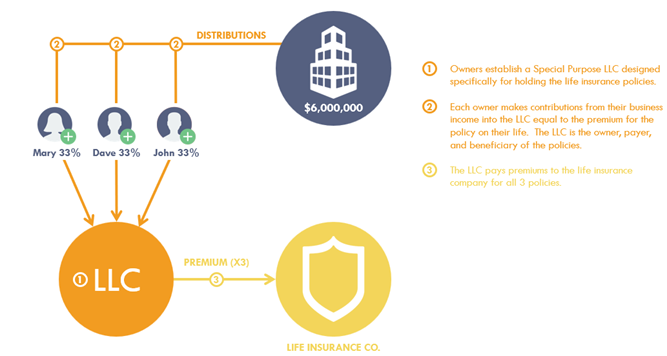

#3 Special Purpose LLC Buy-Sell

An LLC Agreement is also referred to as a Special Purpose Insurance Only LLC. This is a hybrid between the Cross Purchase and the Entity Purchase. It’s technically an Entity Purchase but it’s not the original entity – it’s a standalone entity, giving you the step-up in basis benefit.

Let’s use the same scenario as the Entity Purchase Arrangement with John, Mary, and Dave each owning 1/3 of a company valued at $6,000,000.

Here a separate entity is set up, specifically an LLC, to be the owner of the life insurance policy.

The LLC:

- Owns,

- Pays for, and

- Is the beneficiary of the life insurance policy

Mary, Dave, and John would each own a third of this separate entity – the LLC. From here, they would fund and contribute to the LLC with a corresponding premium.

Now, at death, the insurance company receives the death benefit, the death benefit pays the remaining two owners. They take the money and directly purchase it from John’s estate, which then the $2,000,000 comes back to them. The surviving buyers, Mary and Dave, now receive a step-up in basis from this agreement. Because the policies are held in an LLC, it’s better protected from creditors.

At retirement, which is more than likely to be the outcome, owners of the life insurance policies are transferred to each individual owner. The LLC is dissolved upon retirement and/or exit of all partners. This allows each owner to retain their own policy and repurpose it for potential personal planning needs.

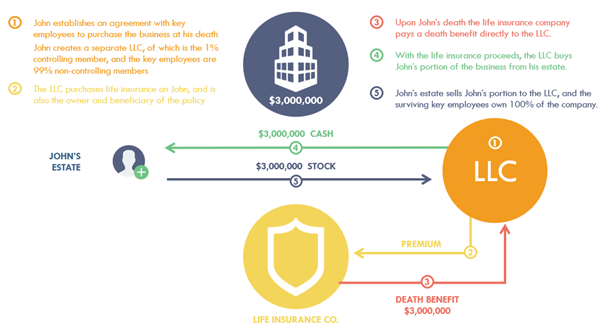

#4 Unilateral Buy-Sell

A Unilateral Buy-Sell is also referred to as a One-Way Buy-Sell. This structure is very similar to the Special Purpose LLC – there is a separate entity but rather than other business owners, key employees are plugged in. They will get the majority of the ownership but none of the voting ownership.

Here the LLC:

- Buys,

- Pays for, and

- Is the beneficiary of the life insurance policy

At John’s death, the money goes into the cash, the death benefit goes into the LLC, it pays out John’s estate, and the stock goes into the LLC whereby the employees become owners of the company.

This structure is ideal for John’s circumstance as a single business owner:

- A simple strategy for a sole owner

- The new owner (key employees) receives a step-up in tax basis

- Seller can structure additional compensation to pay premiums

However, the downsides under this arrangement includes:

- Challenge to find willing and competent participants

When working to find an agreement that is right for you and your unique business situation, it’s of utmost importance that all parties involved have all the information at your disposal. Failing to have an agreement best suited for you can cause unnecessary turmoil.

Implement A More Seamless Buy-Sell Agreement

With so many unknowns in life, Buy-Sell Agreements are valuable (and essential) tools for maintaining control and stability within your business and any unforeseen events. However, these agreements can become increasingly complex as the number of business owners increases.

For this reason, it’s essential to consult with legal and financial professionals to structure and implement the right Buy-Sell agreement and implement it effectively.

To best protect yourself for ever evolving circumstances, let us help you understand how much coverage you need and what your business is worth.

2023-162163 Exp. 9/2025

Material discussed is meant for general informational purposes only and is not to be construed as tax, legal, or investment advice. Although the information has been gathered from sources believed to be reliable, please note that individual situations can vary. Therefore, the information should be relied upon only when coordinated with individual professional advice.